What Our Clients Are Saying

What is Our Best Defense Against Inflation?

Posted on:

September 28, 2020This is a great question. And it’s something a lot of people are wondering about these days. With our country printing literally trillions of dollars in 2020, inflation is going to be a real concern in the coming years.

Put simply, inflation eats away the value of our dollars.

The academic formula that best describes how that happens is MV = TP. Let’s translate that into English.

M is the amount of money in the economy.

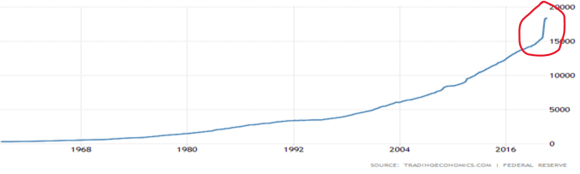

With the recent stimulus bills, the government has increased the money supply by roughly 20% this year. You can see what an unprecedented spike this has been in this chart:

Next, we have V, or the Velocity of money.

Essentially, this is how often each dollar in the economy gets spent each year.

The velocity of money has nose-dived in 2020 because we have all been stuck at home, businesses have been closed, or have been forced to reduce capacity. You can see that the velocity of money is down almost 25% this year:

This lack of velocity is why we have avoided inflation so far in 2020, despite the unprecedented spike in the money supply. Even though there are more dollars in circulation these days, people are not spending those dollars as fast as they were spending last year.

Finally, T stands for the number of Transactions happening in the economy each year and P stands for the Price of everything being bought and sold in the economy.

Money x Velocity = Transactions x Price

If the amount of money in system remains where it is today and the velocity of money and number of transactions returns to where they were pre-COVID, prices will have to rise. Inflation.

Eventually, and maybe sooner than a lot of people think, people will get back to spending the way they did pre-COVID.

Without a plan for how to reduce the money supply and pull all those extra dollar bills out of the system, how can we avoid inflation? And policymakers haven’t even bothered discussing how they might do that.

With a spike in the money supply of 20% in just this year we worry the increase in prices could be significant.

For long term investors, the best way to “hedge” against inflation is to simply use investments that have a history of generating higher returns than inflation.

After all, if inflation makes everything you have to buy more expensive by 3% per year (which it has historically) then you can directly offset that by investing in something that grows your money by 3% as well.

If something you want to buy increases in price from $100 to $103 but at the same time the $100 you want to use to buy is invested and it also grows to $103 then you’ve directly offset the price inflation with your investment return.

We’re even better protected by investing in something that earns 5% or 7% or 10%. The better the rate of return, the more protection you have against inflation.

How About Gold?

There is a very common belief that precious metals in general and gold in particular are the best ways to “hedge” against inflation. After all, if the US Government is debasing the US Dollar by printing trillions more why not get out of that currency? If you hold your money in gold you’re not subject to the ups and downs of the US dollar and therefore you’re money is protected from inflation, right?

If we look at how much an ounce of gold costs in US Dollars after accounting for inflation over time we see a couple of things:

- As an investment, gold did really well from 1971 to 1980. From a low of $35/ounce ($262 in today’s dollars) just before the US went off the gold standard to a high of $843/ounce (more than $2,200 in today’s dollars) – more than 42%/yr. for those 9 years!

- But today the price of gold is less than $2,000/ounce. It was worth more than $2,200/ounce in today’s dollars 40 years ago!

History is Still Our Best Guide

Historically, the two asset classes with the best protection against inflation are stocks and real estate. Stocks have historically averaged 10-12% returns per year, while investment real estate has historically averaged roughly 9% returns per year.

The problem with real estate for most people is they’re usually already overly concentrated in real estate because of their investment in their home.

But once someone has enough assets on their balance sheet to mitigate that, we believe real estate can be an intelligent holding for diversification and beating inflation.

The higher returns and the ability to get thoroughly diversified at very low cost make a diversified portfolio of stocks a better “hedge” against inflation for most people.

Many people will say there is too much “risk” in holding stocks. We explore that topic and more in our new 9-Email Course: Foundations of Financial Success. Sign up here for free!

Disclosure:

Tumwater Wealth Management is a registered investment adviser and may only conduct business in states where it is registered or exempt. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Build a Retirement Income Plan that Gives You Confidence and Freedom

Sign up for our Retirement Income Planning Course.

Learn more